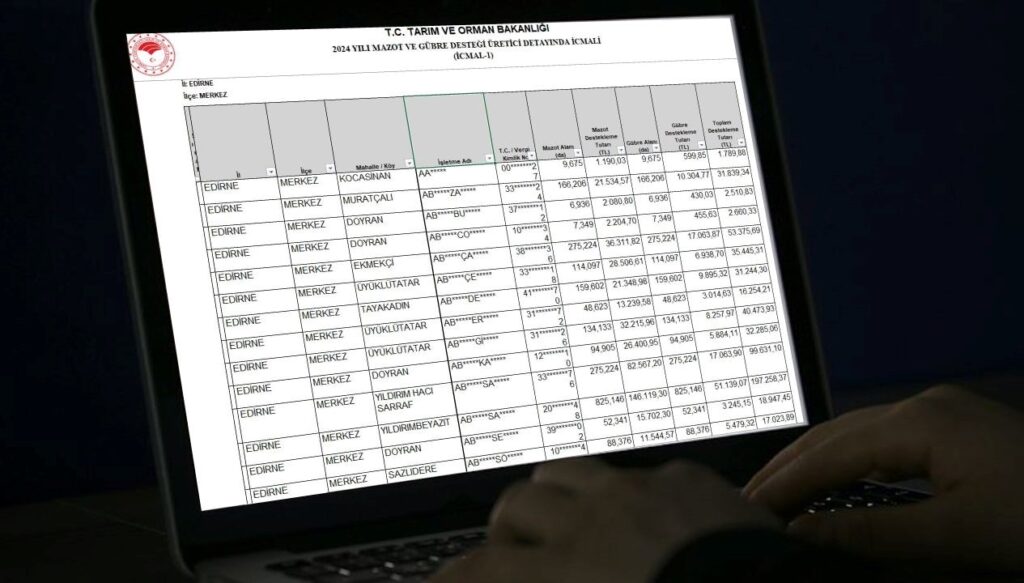

Adjustment of Tobacco Tax for Inflation

The excise tax rate on tobacco has been reduced. To compensate for the decrease in tax revenues resulting from the reduction, the fixed tax amount has been increased. The adjustment was made to limit the inflationary effect. Changes were made in both the excise tax rate and fixed tax amount for tobacco products. The Presidential Decree on the matter was published in the Official Gazette and became effective. EXCISE TAX AND FIXED TAX RATE CHANGED FOR TOBACCO With the decision, the excise tax rate and fixed tax amount for tobacco products were redefined. According to information obtained from the Ministry of Treasury and Finance, changes were made to the composition of the excise tax in a way that would not lead to any changes in tax revenues. In this context, while a reduction was made in the excise tax rate for tobacco products, an increase in the fixed tax amount was carried out to compensate for the decrease in tax revenues resulting from this reduction. AIM TO LIMIT THE INFLATIONARY EFFECT With the regulation, the multiplier effect of tobacco was reduced from 4.4 to 3.8, aiming to support the fight against inflation as a fiscal policy. Therefore, the amount of increase required in tobacco prices due to a 1 lira increase in costs is not 4.4 lira but 3.8 lira. It was noted that this fiscal policy step taken in line with budget targets aims to limit the inflationary effect.