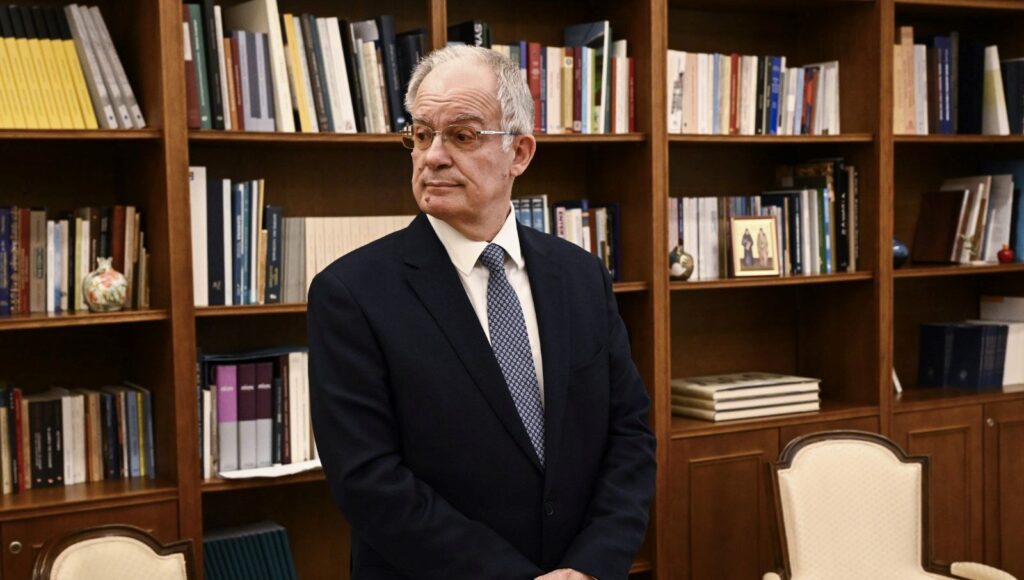

Central Bank Governor Karahan: We Will Do Whatever It Takes to Achieve the Inflation Target

The Governor of the Central Bank of the Republic of Turkey, Fatih Karahan, stated that they will do whatever it takes to reach the 24% inflation target. Karahan emphasized that the switch to the Turkish Lira is higher than the transition to foreign currency.

During his visit to the New York Office of Anadolu Agency (AA) in the United States, Governor of the Central Bank of the Republic of Turkey (CBRT) Fatih Karahan answered questions about the agenda. Karahan evaluated that the recent decline in inflation is due not only to base effects but also to the main downward trend, influenced by a tight monetary policy.

Karahan expressed that the improvement in the main trend will be effective in the remaining months of the year to ensure a decline in inflation, targeting 24% by the end of the year. He emphasized that they will continue their tight monetary policy stance, stating that it is crucial for demand to remain at disinflationary levels for the continuation of the decline in inflation. Karahan pointed out that the transition from individual exchange rate protected deposit accounts to the Turkish Lira is higher compared to the transition to foreign currency. Governor Karahan stressed that while determining the policy rate in the upcoming period, the priority will be to provide the tightness required by the disinflation path, maintaining a tight monetary policy stance until a permanent decrease in inflation and price stability are achieved.

Karahan responded to various questions about combating inflation, monetary and interest rate policies, the transition from exchange rate-protected deposit accounts to the Turkish Lira, and foreign currency loans, stating the following: In January, high inflation was observed but we saw a drop again in February. How should we interpret future inflation data? In Turkey, the annual inflation has been decreasing since the peak in May 2024. We assess that a significant portion of the decline observed in the early months of the disinflation process is due to the base effects caused by developments in the summer of 2023. We were focusing on redirecting expectations regarding the policy rate to monthly price developments to guide them accurately. Therefore, we were examining the trend of seasonally adjusted main indicators for the last few months. At this point, we evaluate that the decrease in inflation is caused by the main downward trend and not just base effects, attributable to the influence of a tight monetary policy. We expect that the improvement in the main trend will be effective in the remaining months of the year. In addition, there are cases where seasonally adjusted methods fail to capture the changing seasonality post-pandemic. When all these factors are considered together, we find it more accurate to compare the main trend indicators with the same month of the previous year. Looking at the main trend indicators for February, the seasonally adjusted B index decreased from 4.3% in 2024 to 2.8% in 2025, and the C index also dropped from 3.7% to 2.4%. As known, these two indexes increase due to temporary factors unrelated to the impact of monetary policy in January, February, and July. In these months, indicators dependent on distribution, like the median and SATRIM, can provide a better idea about the inflation trend. Median price increases decreased from an average of 4.7% in the January-February period last year to 2.1% this year. We also saw a similar decrease in SATRIM. When all these factors are combined, we observe that the monthly main trend has decreased by one-third in the B and C indexes since last year and halved in the median and SATRIM indicators.

“WE WILL DO WHATEVER IT TAKES TO REACH THE TARGET”

To understand the inflation dynamics, it is also beneficial to view inflation on a sub-category level. In terms of annual inflation developments, we perceive that while the inflation in goods remains low, in services, despite the beginning of some fragmentation, the level is still high. Rents and education, which have a high tendency for time-dependent price determination and indexing to past inflation, particularly stand out in this regard. The annual rental inflation decreased from 121% in February last year to 97% this year. In this category, both the level is high and disinflation is slow. We also observe a limited improvement in education. On the other hand, in the service group, we see a significant improvement in items more sensitive to monetary policy. For instance, restaurant and hotel inflation decreased from 95% to 46%. This indicates that monetary tightness is effective in lowering inflation in such service categories. We will do whatever it takes to reach our end-of-year inflation target of 24%. By continuing our tight monetary policy stance, we will continue to reduce inflation in line with our end-of-year targets. We saw a strong demand in the fourth quarter of last year. What does this data mean for the inflation outlook? Before the announcement of the national income data for the fourth quarter, we were following data such as card spending, credit growth, and retail sales to understand demand conditions. These data indicated that demand was somewhat resilient but remained at disinflationary levels in the fourth quarter. The relevant growth data announced at the end of February showed that the demand was stronger than our estimates. Indeed, we emphasized this in the recent MPC statement. It is crucial for demand to remain at disinflationary levels for the continued decline in inflation. In this regard, looking at the data announced for the first quarter, we see that retail sales retained their strength in January, while the volume of automotive and wholesale trade declined. Credit growth is milder compared to the fourth quarter. The data on spending with cards indicate a weaker trend in January and February. Therefore, the current demand indicators for the first quarter imply that consumer spending was more moderate following the increase observed in the previous quarter. We will continue to evaluate this outlook as the demand indicators for the first quarter accumulate. We will not allow demand conditions to disrupt the disinflation process.

“WE DO NOT HAVE A FOREIGN EXCHANGE RATE TARGET” In January, we saw an increase in the current account deficit. Your policy texts continue to emphasize real appreciation in the Turkish Lira. Can you evaluate the real appreciation and current account outlook for 2025? Looking at the developments in the current account, we see that the current account deficit as a percentage of national income decreased from 5% before the tightening to 0.8% at the end of 2024. Considering that the average ratio of the current account deficit to national income was 3.7% over the past